A family trust is commonly a discretionary trust where a trustee holds and manages assets for beneficiaries, usually within the same family group.

Many families use a family trust structure to organise investments, operate a family business, and distribute income in a tax-efficient way. Understanding how these trusts operate, their advantages, and how to set up a family trust is important before establishing this type of trust arrangement.

What is a family trust in Australia?

A family trust in Australia is a legal arrangement where a trustee manages assets on behalf of beneficiaries according to the rules outlined in a trust deed. This structure is commonly used by families to manage wealth, investments, and family businesses. In most cases, a family trust is established as a discretionary trust, meaning the trustee decides how trust income is distributed among beneficiaries each financial year, subject to the trust deed and any required trustee resolutions.

This flexibility allows families to manage shared assets and distribute income based on financial circumstances. For business owners, a family trust may support tax planning by allowing income to be allocated among beneficiaries within the family group, where permitted by the trust deed and tax rules.

How do family trusts work in Australia?

A family trust allows assets to be held by the trustee on trust rather than owned directly by individuals. The trustee manages the trust assets and distributes trust income to beneficiaries according to the rules defined in the trust deed.

In many cases, beneficiaries are assessed on trust income to which they are presently entitled, while the trustee may be taxed in some circumstances, including where income is not effectively distributed. Beneficiaries generally report their share of trust income in their personal tax returns and pay tax based on their marginal tax rates, where they are presently entitled. This structure is widely used by families managing shared investments, property portfolios, or family businesses.

How is trust income distributed?

At the end of each financial year, the trustee decides how trust income will be distributed among beneficiaries within the defined family group, subject to the trust deed and any required trustee resolutions. This decision must comply with the trust deed and Australian tax requirements, including any timing rules for effective resolutions. The trustee considers the circumstances of beneficiaries when determining distributions.

The top marginal tax rate in Australia is 45% plus a 2% Medicare levy, resulting in an effective rate of approximately 47% depending on individual circumstances. Because beneficiaries may have different tax rates, distributing income within the family group may help improve tax efficiency, although outcomes depend on the deed, beneficiary circumstances, and anti-avoidance rules.

Example distribution scenario:

Who pays tax on trust income?

Beneficiaries who are presently entitled to trust distributions are generally responsible for paying tax on their share of trust income. They must include these distributions in their personal tax return and pay tax according to their marginal tax rate. If income is retained rather than distributed, the trustee may be taxed at the top marginal individual rate on undistributed income.

Trustees must ensure distributions and reporting comply with Australian Taxation Office (ATO) requirements, including valid trustee resolutions where applicable.

Tax implications of a family trust in Australia

Tax considerations are one reason families and business owners explore family trust structures. In discretionary trusts, income is usually distributed to beneficiaries each financial year, and those beneficiaries are generally responsible for paying tax on their allocated share if they are presently entitled.

Important tax considerations may include:

- trustee resolutions determining how income is distributed

- beneficiaries reporting distributions in their personal tax returns

- potential distribution of capital gains or franking credits

- the trustee may be taxed at the highest individual marginal rate if income is retained within the trust

- anti-avoidance rules such as Part IVA of the Income Tax Assessment Act 1936

Because trust taxation rules can be complex and vary depending on individual circumstances, families often seek professional advice or guidance from the ATO when making tax planning decisions.

Advantages of a family trust

Many families and business owners consider establishing a family trust because it can offer structural and financial advantages.

Tax planning opportunities

A discretionary trust may allow income to be distributed among beneficiaries with different marginal tax rates, subject to the trust deed and tax law. When managed within tax law requirements, this flexibility may help improve overall tax efficiency across the family group.

Asset protection

Assets held within a trust are held by the trustee on trust rather than by individual family members personally. Depending on the circumstances, this separation may provide some protection from certain business risks or creditor claims, but it is not guaranteed.

Flexibility in managing family assets

A family trust provides flexibility in managing investments and income distributions. Trustees may adjust distributions annually depending on financial circumstances, which can assist families managing investments, property, or business income.

Disadvantages and risks of family trusts

Although family trusts offer potential advantages, they also involve responsibilities and possible risks.

Compliance and tax reporting

Trusts generally must maintain financial records and lodge annual tax returns with the ATO where required. Trustees are responsible for ensuring the trust complies with relevant tax and legal obligations.

Potential family disputes

Because the trustee controls income distributions, disagreements between beneficiaries may arise. Clearly defined responsibilities in the trust deed and transparent communication between family members can help reduce the likelihood of disputes.

Setup and administration costs

Establishing a trust structure requires legal documentation, such as preparing a trust deed and registering the trust for tax purposes. Initial setup costs can vary widely and are often quoted as a market estimate rather than a fixed fee.

Ongoing administration may include accounting services, trust tax returns, and compliance reporting, with annual costs varying by trust complexity and adviser fees.

When a family trust may be suitable

A family trust may be suitable for families who want to manage assets collectively, operate a family business, or plan succession, depending on their tax and legal circumstances.

This structure is often used for:

- managing investment portfolios

- holding property assets

- running family businesses

- distributing income among family members

Family trusts may also support long-term financial planning and succession planning across generations. However, whether a trust structure is appropriate depends on financial circumstances, tax considerations, and compliance requirements. Seeking professional accounting or legal advice may help families determine whether a trust aligns with their financial objectives.

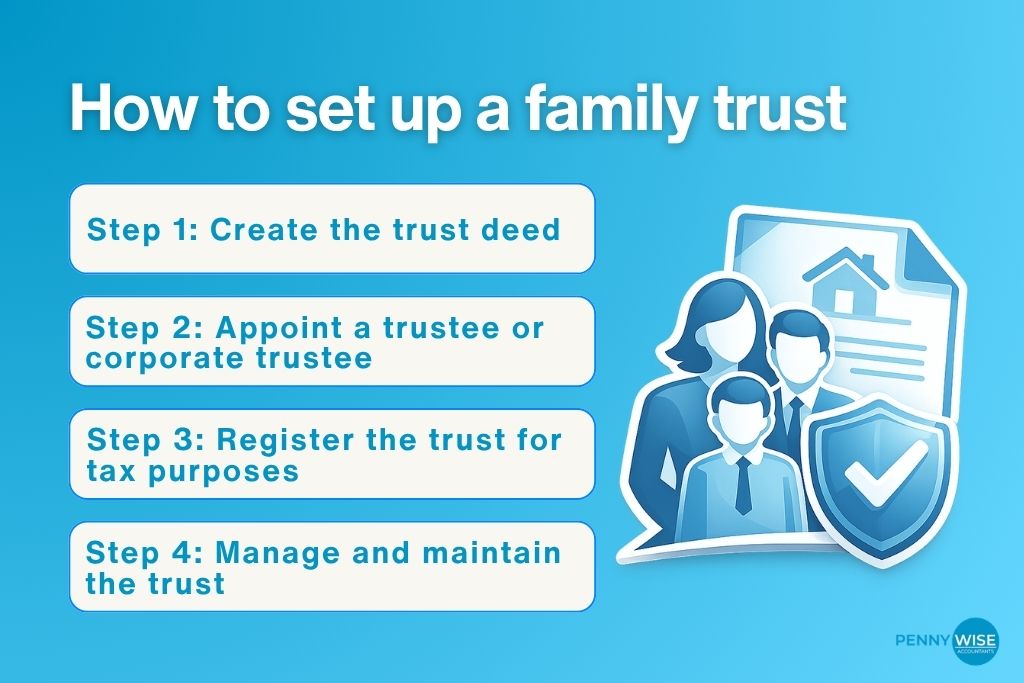

How to set up a family trust

Setting up a family trust involves several key steps to ensure the trust is legally established and compliant with tax requirements.

Step 1: Create the trust deed

The trust deed is the legal document that establishes the trust and outlines how it operates. It identifies the beneficiaries, defines the powers of the trustee, and sets the rules for managing and distributing trust income and assets. Once the deed is properly executed and settled, the trust is formally created.

Step 2: Appoint a trustee or corporate trustee

The trustee is responsible for managing the trust and its assets. This role can be held by an individual or a company acting as a corporate trustee. A corporate trustee is often used to help maintain a clearer separation between personal and trust assets, but it is optional rather than mandatory.

Step 3: Register the trust for tax purposes

After the trust is created, the trustee should arrange the trust’s tax registrations, including a TFN and, if applicable, an ABN. This usually includes applying for a TFN and, where the trust is carrying on an enterprise and is entitled, an ABN.

Step 4: Manage and maintain the trust

Once established, the trustee must manage the trust according to the trust deed and make valid annual distribution decisions where required. This includes keeping financial records, preparing annual accounts, lodging tax returns, and distributing trust income to beneficiaries each year.

Is a family trust the right structure for your situation?

A family trust can be a useful structure for families and business owners who want to manage assets, distribute income, and support long-term financial planning. It offers flexibility in allocating income among beneficiaries while helping organise investments or operate a family business. However, trustees must understand the legal responsibilities and tax obligations involved.

In our work with clients at Pennywise Accountants, we often see families explore trust structures when planning how to manage income, investments, or business activities. Because each situation is different, reviewing the trust deed, tax implications, and compliance requirements is important before making decisions. Understanding how a trust fits within a broader financial strategy can help families make informed choices.

Frequently asked questions

How much does it cost to set up a family trust in Australia?

Setting up a family trust may cost around this range in the market, but the actual cost depends on the trust deed, legal work, and whether a corporate trustee is used. Ongoing administration and accounting costs vary depending on the trust’s complexity and adviser fees.

Can a family trust own property or business assets in Australia?

Yes, a family trust can own property, shares, or business assets through the trustee acting on behalf of the trust. Many families use trusts to hold investment properties, share portfolios, or operate family-owned businesses.

What is the difference between a family trust and a company?

A family trust generally distributes income to beneficiaries who may be assessed on their share where they are presently entitled. A company pays tax on its profits before distributing dividends to shareholders. Trusts offer flexibility in income distribution, while companies operate under a fixed ownership structure.

Can the trustee of a family trust be changed?

Yes, the trustee can usually be replaced if the trust deed allows it, and the appointor or equivalent control mechanism often governs the process.

Do family trusts need to lodge tax returns every year?

Yes, family trusts generally lodge annual trust tax returns where required, and the return reports income, expenses, and distributions.

Can a family trust continue after the original trustee dies?

Yes, a family trust can continue operating after the original trustee passes away. The trust deed usually specifies how a new trustee can be appointed to ensure the trust continues managing assets.

Can children receive income from a family trust?

Children can be beneficiaries of a family trust, but special tax rules apply to minors under 18. Under Division 6AA of the Income Tax Assessment Act 1936, unearned income above certain thresholds may be taxed at higher rates unless an exception applies.

How long does a family trust last in Australia, and what does the trust deed say about the vesting date?

A family trust operates until its vesting date, which depends on the trust deed and applicable state or territory law; in many cases the period may be long, but it is not universally 80 years across Australia.

Get a personal consultation.

Call us today at 0405 667 350

Fast responses, clear advice, and tailored solutions for Sunbury individuals and small businesses.